The Housing Machine

Week ending Friday 8 May 2026

Australia’s economy increasingly runs through one giant machine.

Housing.

Australia once rode on the sheep’s back. Today, it runs on residential property.

At roughly $12.6 trillion, Australian housing is now worth about 55% more than the entire ASX and superannuation system combined.

More than half of household wealth sits inside residential property alone.

That changes how the country behaves.

Policy changes.

Rate expectations respond.

Migration settings change.

incentives change.

Because once housing becomes systemically important…

the machine has to keep moving.

This week’s headlines all pointed toward the same underlying reality:

rates,

migration,

housing shortages,

government spending,

future rate cuts,

construction bottlenecks,

investor policy debates.

Different stories.

Same machine.

Because once residential housing reaches $12.6 trillion in value and accounts for more than half of household wealth…

housing stops being just another market.

It becomes systemic.

Feeding The Machine

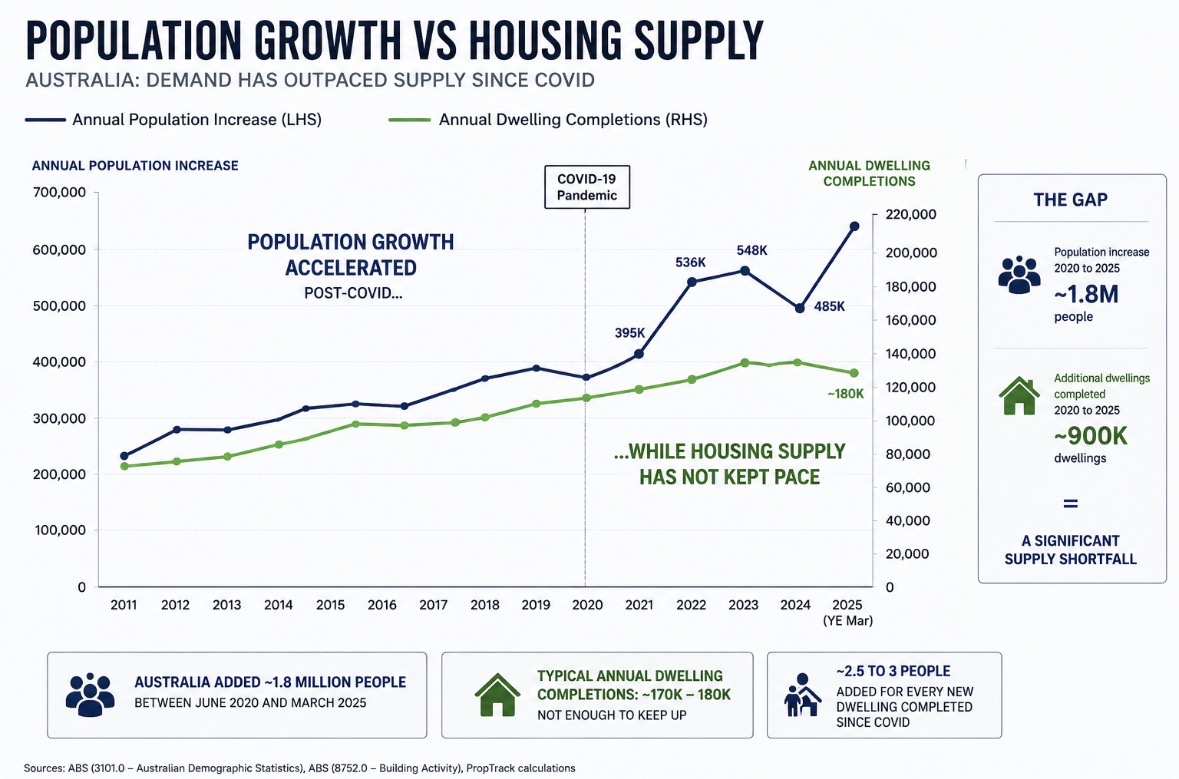

Australia’s population growth since Covid has been among the fastest in the developed world.

Between 2020 and 2025, Australia added roughly 1.8 million people.

At one point, annual population growth exceeded 650,000 people a year.

Meanwhile housing completions have NOT kept pace.

Australia typically builds: roughly 170,000–180,000 dwellings annually

Yet population growth at recent levels implied demand for substantially more.

Australia added roughly:

2.5 to 3 people

for every

new dwelling completed

during the recent surge period.

The pressure eventually surfaces somewhere:

rents,

prices,

infrastructure,

affordability,

or household debt.

The machine keeps moving.

But the strain builds underneath it.

More people:

increase labour supply,

increase tax receipts,

increase consumption,

increase rental demand,

and increase housing demand.

Migration acts a little like an economic sugar hit.

It works quickly.

More people arrive.

More people work.

More people consume.

Tax receipts rise.

Retail spending lifts.

Rental demand increases.

Headline GDP improves.

The machine responds almost immediately.

Lifting productivity is slower work.

That takes infrastructure.

Training.

Technology.

Faster approvals.

Better systems.

More efficient construction.

Those things compound over years, not quarters.

And this is where the housing machine starts becoming increasingly complex to operate.

In a naturally balanced economy, growth tends to regulate itself more organically.

Supply responds.

Demand cools.

Capital reallocates.

Prices send signals.

Australia’s housing system increasingly behaves differently.

The machine now requires constant adjustment just to keep running smoothly.

Rates move.

Migration settings change.

Government spending expands.

Infrastructure programs accelerate.

Investor incentives remain protected.

Planning rules get rewritten.

Housing targets get announced.

Teams of policymakers are effectively standing around the engine bay each month adjusting pressure valves to keep the system turning over.

Because the machine became very large.

At $12.6 trillion, housing now sits underneath household wealth, consumer confidence, bank lending, state revenues, construction activity and large parts of the broader economy itself.

Which means slowing the machine carries consequences far beyond property prices.

And that is where the tension now sits.

The economy increasingly depends on a system that also requires continual intervention to stabilise.

More fuel.

More tuning.

More calibration.

More policy support.

The challenge is that each adjustment often creates pressure somewhere else.

Higher migration supports growth while tightening housing supply.

Lower rates support borrowing while lifting asset prices.

Government spending supports activity while adding inflation pressure.

Planning reform helps supply while infrastructure struggles to keep pace.

The machine must keep running.

But it no longer feels entirely self-sustaining.

And that changes the environment operators are working in.

Productivity Is Becoming The Edge

The interesting part of this cycle is that the opportunity increasingly sits in efficiency.

Faster approvals.

Cleaner projects.

Simpler renovations.

Shorter hold periods.

Modular construction.

Tighter execution.

Because when housing becomes deeply embedded inside the broader economy…

time itself becomes expensive.

Operator Takeaway

Markets respond to incentives.

And Australia’s incentives increasingly revolve around keeping the housing machine operating smoothly.

That creates pressure.

Which leads to distortions.

And in turn, necessitates intervention.

All of this surfaces opportunities for operators who understand where the friction points are emerging.

Because this environment increasingly rewards:

productivity,

speed,

adaptability,

and disciplined execution.

The easy gains from broad liquidity already happened.

This phase of the cycle looks more selective.

More operational.

More dependent on execution than momentum.

And that changes where the edge sits.

Inside Proptix, we’re tracking:

stock on market

days on market

vendor pressure

supply-demand imbalance

liquidity shifts

renovation feasibility

time-risk exposure

So operators can identify where the machine is tightening…

before it fully flows through to price.